A Total-Package Offering Inside the APP Annuity

The APP annuity is rich in performance-based features that are designed to be a strong addition to any agent portfolio or client plan.

5% Premium Bonus

Policyholders will receive a one-time premium bonus of 5% with or without the selection of the Rate Enhancement Rider! The premium bonus is immediately credited to your account, increasing the value of your account and giving you the opportunity to earn additional interest. Premium Bonus is subject to a vesting schedule.

Same Great Guarantees

Participation rates are guaranteed for 10 years1 from the annuity issue date with the selection of the Momentum Index and Diversified Macro 5 Index 1- and 2-year point-to-point crediting strategies! These guarantees help build confidence by locking in rates for ten years, avoiding renewal rate uncertainty, unexpected rate decreases, and gives more reliability in the strategy because it will deliver on its promises.

Consistent Rate History

APP annuity rates have steadily increased since launch across all strategy options. This is backed by our Rate Integrity Philosophy.

Flexible Crediting Strategies

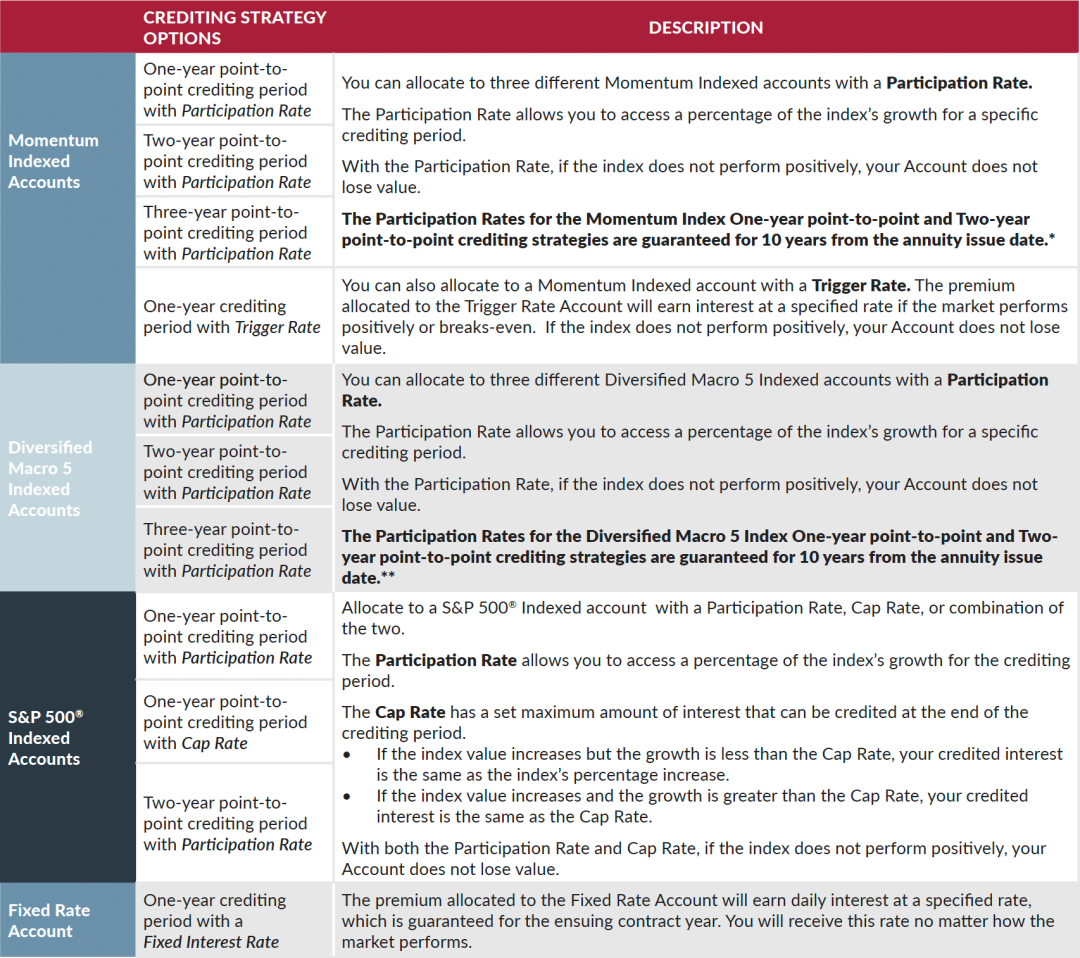

Multiple index strategy options, a fixed rate, trigger rate, and cap rate are available to choose from for accumulation needs. Ten indexed accounts are linked to three different indices, the Momentum Index, Diversified Macro 5 Index, and the S&P 500®.

Additionally, an optional Rate Enhancement Rider is available to add more value.

1 The Participation Rates for the Momentum Index One-year point-to-point and Two-year point-to-point crediting strategies are guaranteed for 10 years from the annuity issue date, provided that Sentinel Security Life Insurance Company continues to have access to the Momentum Index. The Participation Rates for the Diversified Macro 5 Index One-year point-to-point and Two-year point-to-point crediting strategies are guaranteed for 10 years from the annuity issue date, provided that Sentinel Security Life Insurance Company continues to have access to the Diversified Macro 5 Index.

Choose from Eleven Growth Strategies

Choose how the annuity premium is allocated across eleven crediting strategies. These crediting strategies include a Fixed Account and ten Indexed Accounts linked to three indices, the Momentum Index, the Diversified Macro 5 Index, and the S&P 500® Index.

Adjust allocations on the contract anniversary that coincides with the end of each strategy’s crediting period. At that time, the option to allocate to any available strategy for a new crediting period of one, two or three years is available.

Did you know? The APP annuity’s Trigger Rate may be a good alternative for clients considering Fixed Rate allocations.

How the Trigger Rate works: if the Momentum Index earns 0% or more, then the premium allocated to the Trigger Rate account will earn interest at a specified rate of 9% for the base product and 11% with the rider.

So, the benefit of the Trigger Rate is that it earns a higher rate than as long as the Momentum Index breaks even or earns a positive return.

Optional Rate Enhancement Rider

An optional Rate Enhancement Rider2 offers more benefits to policyholders:

- Higher Rate Options: higher Participation, Cap, Trigger, and Fixed Rates for more growth potential.

- More Liquidity: Increases the free withdrawal amount to 10%, after the first contract year.

- Pricing Guarantee: 110% Return of Premium (ROP) Guarantee if the Rate Enhancement Rider is purchased and the contract remains in force for 10 years. Please note: premium is adjusted for withdrawals.

2 There is a fee with the purchase of the rider.

Accumulation with Accessibility

Free withdrawals

Some annuities do not offer free early withdrawals, but in the second contract year, the APP annuity allows clients to withdraw up to 5% of their Account Value or Required Minimum Distribution, whichever greater.

Terminal Illness and Nursing Home Waiver

If the annuity owner is diagnosed with a terminal illness or needs to move into a nursing home, he or she can make a full surrender or partial withdrawal without a Market Value Adjustment, Surrender Charge, or loss of any applicable Non-Vested Premium Bonus under certain conditions.

Additional Features

Premium Bonus Vesting Schedule

When your client purchases the Accumulation Protector PlusSM Annuity they will receive a one-time premium bonus of 5%. The premium bonus is immediately credited to the policyholder’s account, increasing the value of their account and giving them the opportunity to earn additional interest. The policyholder’s funds can be accessed subject to their vesting schedule.

Surrender Charge Schedule

If your client surrenders their policy or requests withdrawals above the penalty-free amount, there may be surrender charges. Policyholders should discuss the surrender charge schedule with their agent.

Death Benefit Settlement Option

Protect loved ones with the APP’s Death Benefit feature. If the annuity owner passes away before receiving any proceeds3, other than a Withdrawal, the amount payable to beneficiary(ies) is equal to the greater of the Account Value less any Non-Vested Premium Bonus or the Minimum Guaranteed Surrender Value determined as of the date of death.

3Proceeds are defined as the amount payable when: (1) the Owner takes a Withdrawal; (2) the Owner surrenders their Contract; (3) an Owner dies; or (4) the Contract matures.

Product Sites

Quick Links

For Sentinel Security Life Insurance Company-Licensed Agent Use Only.

All product recommendations must be prioritized by the consumer’s best interest.

This website is intended only for the person or entity to which it is addressed and may contain confidential and/or privileged material. Please be aware that any unauthorized review; copying, use, disclosure or distribution of this information is prohibited.

The “S&P 500® ” is a product of S&P Dow Jones Indices LLC or its affiliates (“SPDJI”), and has been licensed for use by Sentinel Security Life Insurance Company. Standard & Poor’s® and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”); and these trademarks have been licensed for use by SPDJI and sublicensed for certain purposes by Sentinel Security Life Insurance Company. Accumulation Protector PlusSM Annuity is not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P® , or their respective affiliates, and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or interruptions of the S&P 500® .

The Momentum Index and Diversified Macro 5 Index are volatility-controlled indexes that may include a fee in the computation of the index value.

MerQube/Diversified Disclaimer: Neither MerQube, Inc. nor any of its affiliates (collectively, “MerQube”) is the issuer or producer of Accumulation Protector PlusSM Annuity and MerQube has no duties, responsibilities, or obligations to purchasers of the Accumulation Protector PlusSM Annuity. The index underlying the Accumulation Protector PlusSM Annuity is a product of MerQube and has been licensed for use by Sentinel Security Life Insurance Company. Such index is calculated using, among other things, market data or other information (“Input Data”) from one or more sources (each such source, a “Data Provider”). MerQube® is a registered trademark of MerQube, Inc. These trademarks have been licensed for certain purposes by Sentinel Security Life Insurance Company in its capacity as the issuer of the Accumulation Protector PlusSM Annuity. Accumulation Protector PlusSM Annuity is not sponsored, endorsed, sold or promoted by MerQube, any Data Provider, or any other third party, and none of such parties make any representation regarding the advisability of investing in securities generally or in Accumulation Protector PlusSM Annuity particularly, nor do they have any liability for any errors, omissions, or interruptions of the Input Data, Diversified Macro 5 Index, or any associated data. Neither MerQube nor the Data Providers make any representation or warranty, express or implied, to the owners of the Accumulation Protector PlusSM Annuity or to any member of the public, of any kind, including regarding the ability of the Diversified Macro 5 Index to track market performance or any asset class. The Diversified Macro 5 Index is determined, composed and calculated by MerQube without regard to Sentinel Security Life Insurance Company or the Accumulation Protector PlusSM Annuity. MerQube and Data Providers have no obligation to take the needs of Sentinel Security Life Insurance Company or the owners of Accumulation Protector PlusSM Annuity into consideration in determining, composing or calculating the Diversified Macro 5 Index. Neither MerQube nor any Data Provider is responsible for and have not participated in the determination of the prices or amount of Accumulation Protector PlusSM Annuity or the timing of the issuance or sale of Accumulation Protector PlusSM Annuity or in the determination or calculation of the equation by which Accumulation Protector PlusSM Annuity is to be converted into cash, surrendered or redeemed, as the case may be. MerQube and Data Providers have no obligation or liability in connection with the administration, marketing or trading of Accumulation Protector PlusSM Annuity. There is no assurance that investment products based on the Diversified Macro 5 Index will accurately track index performance or provide positive investment returns. MerQube is not an investment advisor. Inclusion of a security within an index is not a recommendation by MerQube to buy, sell, or hold such security, nor is it considered to be investment advice.

NEITHER MERQUBE NOR ANY OTHER DATA PROVIDER GUARANTEES THE ADEQUACY, ACCURACY, TIMELINESS AND/OR THE COMPLETENESS OF THE DIVERSIFIED MACRO 5 INDEX OR ANY DATA RELATED THERETO (INCLUDING DATA INPUTS) OR ANY COMMUNICATION WITH RESPECT THERETO. NEITHER MERQUBE NOR ANY OTHER DATA PROVIDERS SHALL BE SUBJECT TO ANY DAMAGES OR LIABILITY FOR ANY ERRORS, OMISSIONS, OR DELAYS THEREIN. MERQUBE AND ITS DATA PROVIDERS MAKE NO EXPRESS OR IMPLIED WARRANTIES, AND THEY EXPRESSLY DISCLAIM ALL WARRANTIES, OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE OR AS TO RESULTS TO BE OBTAINED BY SENTINEL SECURITY LIFE INSURANCE COMPANY, OWNERS OF THE ACCUMULATION PROTECTOR PLUSSM ANNUITY, OR ANY OTHER PERSON OR ENTITY FROM THE USE OF THE DIVERSIFIED MACRO 5 INDEX OR WITH RESPECT TO ANY DATA RELATED THERETO. WITHOUT LIMITING ANY OF THE FOREGOING, IN NO EVENT WHATSOEVER SHALL MERQUBE OR DATA PROVIDERS BE LIABLE FOR ANY INDIRECT, SPECIAL, INCIDENTAL, PUNITIVE, OR CONSEQUENTIAL DAMAGES INCLUDING BUT NOT LIMITED TO, LOSS OF PROFITS, TRADING LOSSES, LOST TIME OR GOODWILL, EVEN IF THEY HAVE BEEN ADVISED OF THE POSSIBILITY OF SUCH DAMAGES, WHETHER IN CONTRACT, TORT, STRICT LIABILITY, OR OTHERWISE. THE FOREGOING REFERENCES TO “MERQUBE” AND/OR “DATA PROVIDER” SHALL BE CONSTRUED TO INCLUDE ANY AND ALL SERVICE PROVIDERS, CONTRACTORS, EMPLOYEES, AGENTS, AND AUTHORIZED REPRESENTATIVES OF THE REFERENCED PARTY.

Attributions and Disclaimers with Respect to UBS AG: MERQUBE, INC. (“MQ”) is the sponsor of the Diversified Macro 5 Index. MQ has contracted with UBS AG or one of its affiliates (collectively, “UBS”) to license the use of the Global Equity Market 10% RC Index, UBS FX EM9 Momentum ER Index, UBS Global 26 FX Carry Excess Return Index, UBS Bond Futures Trend Index, UBS Commodities Custom Curve 145 Index, UBS Commodities Custom Trend x AL x Oil Index, and UBS CMCI Components Emissions Hedged USD Excess Return (collectively, the “UBS Indices”) in connection with the Diversified Macro 5 Index. The Diversified Macro 5 Index and Accumulation Protector PlusSM Annuity are not in any way sponsored, endorsed or promoted by UBS. UBS has no obligation to make any consideration in composing, determining or calculating the UBS Indices (or causing the UBS Indices to be calculated). In addition, UBS makes no warranty or representation whatsoever, express or implied, as to the results to be obtained from the use of the UBS Indices and/or the level at which the UBS Indices stands at any particular time on any particular day or otherwise. UBS shall not be liable, whether in negligence or otherwise, for any errors or omissions in the UBS Indices or in the calculation of the UBS Indices or under any obligation to advise any person of any errors or omissions therein. UBS shall not be liable for the results obtained by using, investing in, or trading the Diversified Macro 5 Index or Accumulation Protector PlusSM Annuity.

The Momentum Index, (the “Index”), and any trademarks, service marks and logos related thereto are service marks of Solactive AG (“Solactive”). Solactive has no relationship to Sentinel Security Life Insurance Company, other than the licensing of the Momentum Index and its service marks for use in connection with the Accumulation Protector PlusSM Annuity and is not a party to any transaction contemplated hereby. The Accumulation Protector PlusSM Annuity is not sponsored, endorsed, or promoted by Solactive in any way and Solactive makes no express or implied representation, guarantee or assurance regarding the quality, accuracy and/or completeness of the Index, and the results obtained or to be obtained by any person or entity from the use of the Index. Solactive reserves the right to change the methods of calculation or publication with respect to the Index. Solactive shall not be liable for any damages suffered or incurred because of the use (or inability to use) of the Index. Solactive shall not be liable for the results obtained by using, investing in, or trading the Accumulation Protector PlusSM Annuity. Solactive has not created, published, or approved this document and accepts no responsibility or liability for its contents or use. Obligations to make payments under the Accumulation Protector PlusSM Annuity are solely the obligation of Sentinel Security Life Insurance Company and are not the responsibility of Solactive.

For Sentinel-Licensed Agents Only